Updated on – 29 Aug 2022

During this Covid -19 pandemic time, the economic condition of the country is under stress. Most of the business sectors are under deep stress and also the job security has reduced drastically. This both things are restricting the money rotation in market.

To ease the stress level especially on the business sector and to circulate the cash flow in the market the RBI is regularly reducing the repo rate which is directly hitting the interest rate of bank and other deposit schemes.

Reduction of interest rate on Secured Investment Schemes

All bank fixed deposit schemes and post office schemes are comes under secured investment option where returns are very much secured and fixed. You will get assured amount after investment tenure.

Before Covid -19 period the bank interest rate was around 6.5-7.5% per annum and post office schemes interest rates ranging from 7-8% per annum which have now reduced down to 5 – 5.5 % and 5.6-6.8% per annum respectively. This sudden drop of interest rate on fixed deposit schemes have reduced the return on investment drastically and interest rate on deposit schemes may further reduce.

As the economic condition is under stressed many other investment option like medium risk investment & Risk Investment option looks very risky. In present market condition investment in stocks, equities and mutual funds are also at high risk and even your invested principle amount can also be on risk.

So in present condition if your return on investment are less but this time priority should be investment to be made in secured investment options and after maturity it can give assured returns.

If you compare the bank deposit schemes and post office deposit schemes, you will find that return on invest on post office schemes are more as compare to bank deposit schemes.

Which one is better ?

Bank deposit schemes or Post office schemes ?

Almost all of the bank deposit schemes have no lock-in-period so you can invest money for emergency and money for security in bank deposit schemes. In case of any emergency the invested money can be withdraw any time with little interest penalty. Although the interest rates of bank deposit schemes are low but it can fetch around Rs 425 – Rs 500 per month per lakh of investment considering yearly yield.

If you are looking to investment for good returns then post office schemes are fetching much better returns on investment as compare to bank deposit schemes.

In non-lock-in post office schemes the interest rate are little higher than the bank deposit schemes but if investment can be made in long term post office schemes having lock-in period of 5-7 years then returns are much higher as compare to bank deposit long term schemes. It can fetch around Rs 460 – Rs 680 per month per lakh of investment considering yearly yield.

Which post office investment plan is best ?

If you compare any bank plans with post office investment plans you will find the post office investment schemes are better specially NSC ( National Saving Certificate ) where lock is 5 years and it is giving assured returns on your investment after completion of tenure.

Also while doing NSC the applicable interest rate is fixed for 5 years so it will give fixed maturity amount. Presently the NCS interest rates is fetching around Rs 650 per month per lakh of investment considering yearly yield.

In present market scenario NSC is the best option to fetch reasonable return and same time the investment is well secured.

More about NSC

National Saving Certificate VIII issue – 5 years scheme is giving good return on investments segment of period 5 years. This scheme is best under secured investment option with 5 year lock-in-period which is giving best returns on investments. Even after maturity, investment can be done for further 5 years period or as scheme available at the time of maturity.

The interest rate offered by post office for this scheme is little less than PPF but PPF has restriction of investment amount of 1.5 Lakhs per financial year but in NSC there is no restriction on investment. You can invest as much money.

Salient Features

Duration – 5 years ( Lock -In )

Minimum contribution – Rs 1000/-

Maximum contribution – No Limit ( Multiple of Rs 100/- )

Interest rate – 6.8% per annum compounded annually

Interest after maturity – Taxable

80C benefit – Yes

- Certificate may be purchased by

(i) a single adult

(ii) Joint A Account (Maximum 3 adults)

(ii) Joint B Account (Maximum 3 adults)

(iv) Minor above 10 years of age

(iv) An adult on behalf of a minor.

(v) A guardian on behalf of a person of unsound mind - Deposits qualify for tax rebate under Sec. 80C of IT Act.

- The interest accruing annually but deemed to be reinvested under Section 80C of IT Act.

- In case of NSC VIII , transfer of certificates from one person to another can be done only once from date of issue to date of maturity.

- At the time of transfer of Certificates from one person to another, old certificates will not be discharged. Name of old holder shall be rounded and name of new holder shall be written on the old certificate and on the purchase application (in case of non CBS Post offices) under dated signatures of the authorized Postmaster along with his designation stamp and date stamp of Post office.

How to Invest in NSC

As online facility is not available for NSC so you can go to your nearest post office where NSC making facility is available. Most of the post office branches are having facility to make NSC.

Check more about NSC and “How to Invest in NSC at Post office”

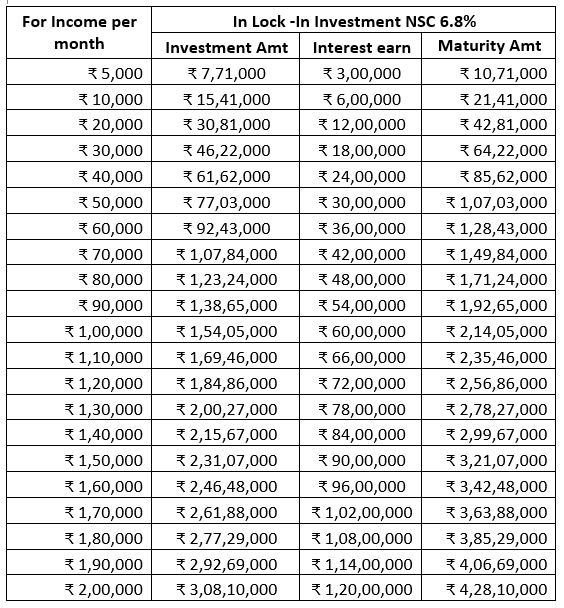

How much you can earn by NSC

You can invest available amount in NSC. Also if you are planning for to secure your fix income then you can invest amount based on how much you want to earn in a month till further five years.

Based on the table you can make investment in NSC.

Advantages & Disadvantages in NSC

Advantages

- NSC is one of the best investment tool which is giving good returns on investments.

- Lock-in-period is reasonable hence it is most popular.

- Interest rate will remain same at the time of purchasing NSC for full tenure of 5 years.

- Return on investment is fixed from first day.

- Loan is available against NSC.

- It can be transfer one time to another person.

Disadvantages

- Due to lock-in-period the money cannot be withdraw in case of emergency.

- The interest earn is taxable.

- Auto renew facility is not available.

- Presently it cannot be made online.

We are well aware the present economic condition due to Covid -19 is improving slowly. It may take longer period so investing in NSC is well secured option and giving reasonable return on our investments.

Well explained sir ????????.